North American MYGAs – Guarantee Choice 3, 5, 7 and 10

Here are a few highlights for the Guarantee Choice MYGA product line:

Issue ages 0-90

Minimum premium of $10,000 non-qualified and $2,000 qualified – high-band rates start at $100,000

Penalty-free withdrawals – access to the earned interest after Year 1, must be at least a $50 withdrawal

Nursing home confinement waiver is included – after Year 1, you can take out 10% of the accumulation value each year

North American BenefitSolutions FIA – 10 and 14 Years

Here are a few highlights for the BenefitSolutions FIA product line:

Issue ages 40-79 on the 10-year and 40-75 on the 14-year (except in CA where the max age is 54)

Minimum premium of $20,000 non-qualified and qualified

Penalty-free withdrawals – access to 5% after Year 1 with a max of 10% if you didn't take any withdrawals the previous year

Rider charge: 1.2% of the benefit base

Benefit base:

Benefit base, less any proportional adjustments for partial surrenders, plus benefit base increases, and never less than the benefit base floor adjusted for partial surrenders

Benefit base floor: In years 1-5: 120% of premium, less any proportional adjustments for partial surrenders;

In years 6-10: 140% of premium, less any proportional adjustments for partial surrenders;

In years 11+: 160% of premium, less any proportional adjustments for partial surrenders

Benefit base increase: Each year for the first 20 Contract years, 100% of the weighted average percentage change in the fixed and indexed accounts.

Interest crediting methods:

Fixed

Annual Point-to-Point with Cap Rate

Annual Point-to-Point with Margin

Monthly Point-to-Point with Cap Rate

Monthly Average with Participation Rate

North American Income SPIA – 5-9 Certain

Issue ages:

Life options: 0-85 (qualified and non-qualified)

Period certain options: 0-93 (qualified and non-qualified)

Note: Issue age plus period certain may not exceed 98 for any period certain only, life with period certain, or joint life with period certain payout option.

Minimum single premium: $25,000 Q or NQ

Maximum premium: $1M

Annuity payout options:

Period certain only: This option provides income for a fixed number of years (ranging from five to 20 years). If the annuitant passes away during that time, payments would continue.

Single life only: Payments are only during the life of the annuitant. If the annuitant passes away, no further payments are made to an estate or any other person.

Single life and period certain: Selecting this option provides income for the life of the annuitant – with a guaranteed payment period (ranging from five to 20 years). If the annuitant passes away before the period ends, payments will continue for the remainder of that period.

Single life with installment refund: This option guarantees that payments will continue during the life of the annuitant. After the annuitant passes away, payments continue until the total payments are equal to the single premium originally paid.

Single life with cash refund: Payments are only during the life of the annuitant. If the annuitant passes away before the total payments received equal the premium, a lump-sum payment is made equaling the difference between the original single premium and any payments already received.

Joint life with survivorship: Selecting this option creates an income stream paid for the life of the annuitant and the lifetime of his or her spouse. After the annuitant passes away (or his or her spouse), payments continue for the remainder of the surviving spouse’s life.

Joint life with survivorship and period certain: This option provides income for the annuitant and his or her spouse’s lifetime – with a guaranteed payment period (ranging from five to 20 years). Should the annuitant or his or her spouse pass away, payments continue for the remainder of the surviving spouse’s life. If both annuitants pass away before the period ends, payments will continue for the remainder of the period.

North American IncomeChoice 10 FIA

Here are a few highlights for the IncomeChoice FIA:

Issue ages: 40-79

Minimum premium (flexible premium): $20,000 NQ and Q

Penalty-free withdrawals – up to 5% after Year 1

Interest crediting strategies:

Fixed

Annual Point-to-Point with Cap Rate

Annual Point-to-Point with Margin

Monthly Point-to-Point with Cap Rate

Annual Point-to-Point with Participation Rate

Annual Point-to-Point with Threshold Participation Strategy

Two Year Point-to-Point with Margin

Included at no additional cost:

Top-tier income potential

GLWB stacking roll-up credit of 2% of GLWB value + stacking potential (150% of dollar amount of interest credited to the accumulation value)

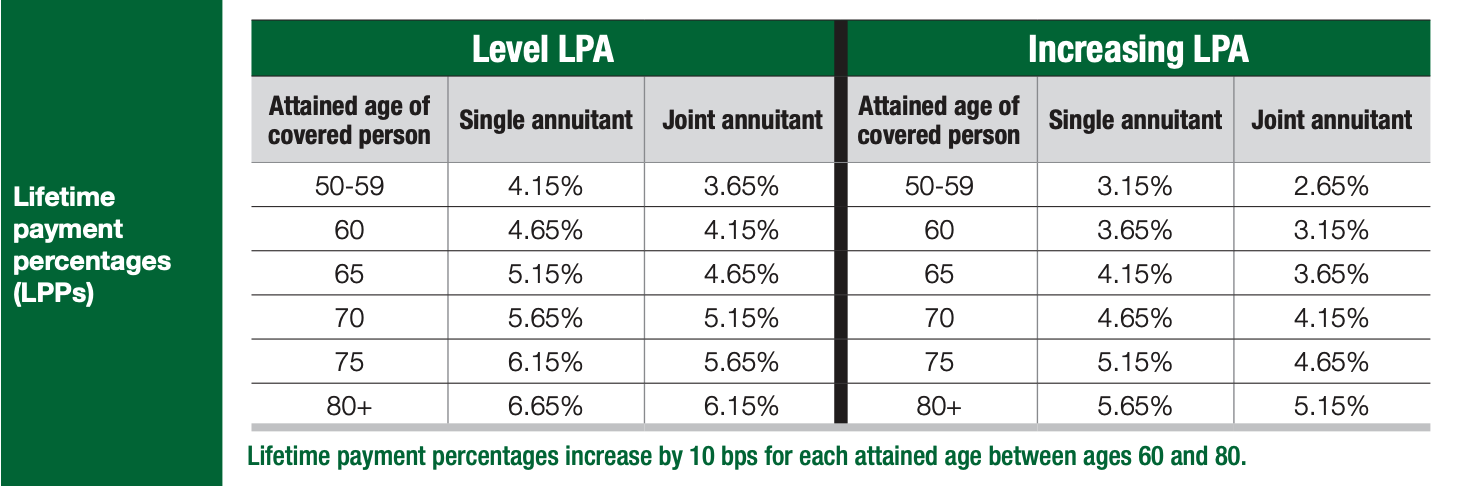

Lifetime payment amount (LPA) feature

Increasing or level LPA options

Required minimum distributions (RMDs) can be taken penalty-free by current company practice

5% GLWB value bonus

North American RetireChoice 10 FIA

Here are a few highlights for the RetireChoice FIA:

Issue ages: 0-79

Minimum premium (flexible premium): $20,000 NQ and Q

Additional premium bonus: 2.5% additional premium bonus which increases from 2% to 4.5% on any premiums received in the first five contract years.

Additional payout benefit: If an annuity payout option is elected after the surrender charge period has elapsed, a 5% bonus will be added to the accumulation value.

Return of premium: At any time in the third contract year and thereafter, the contract may be terminated and the client receives no less than the contract’s net premium paid. The net premium is equal to the initial and subsequent premiums (less any premium bonus and optional rider cost, if applicable, excluding the additional benefit rider cost) minus any withdrawal amounts received (after any surrender charges or interest adjustment).

Enhanced Penalty-Free Withdrawals: 10% of accumulation value after the first year. Beginning the third year, withdrawals can increase to 20% (maximum) if no withdrawal was taken in the previous year. If any penalty-free withdrawal is taken during a contract year, the penalty-free allowance available for the following year resets to 10%. Withdrawals from a contract may decrease the death benefit.

North American VersaChoice 10 FIA

Here are a few highlights for the VersaChoice FIA:

Issue ages: 0-79

Minimum premium (modified single premium): $20,000 NQ and Q

Penalty-free withdrawals – up to 10% after the issue date

Interest crediting strategies:

Fixed

Annual Point-to-Point with Cap Rate

Annual Point-to-Point with Index Margin

Annual Point-to-Point with Participation Rate

Monthly Point-to-Point with Cap Rate

Two-year Point-to-Point with Participation Rate

Optional riders (they do cost):

Enhanced penalty-free withdrawals: Beginning in the second year, up to 20% of the beginning-of-year accumulation value penalty-free if no withdrawals, other than rider charges, were taken in the prior year.

Return of premium: Any time after the second contract year, the client may terminate the contract and receive no less than the contract’s net premium paid. Net premium is equal to initial and subsequent premiums minus any withdrawal amounts, excluding the rider cost, after any surrender charges or market value adjustment.

ADL-based surrender charge waiver: If client is unable to complete two of the six activities of daily living (ADLs) after the issue date and otherwise qualifies, it’s possible to get up to 100% of accumulation value immediately with no surrender charges.

ADL-based payout benefit: After the second contract anniversary, if a client is unable to complete two of the six ADLs and otherwise qualifies, they may choose to draw an income over five years that is based on an enhanced accumulation value amount (percentage varies by contract year, see chart). This accumulation value multiplier increases the longer money is kept in the annuity, maxing out after six years.

North American Charter Plus FIA – 10 and 14 Years

Here are a few highlights for the Charter Plus FIA:

Issue ages: 0-79 for 10-year, 0-75 for 14-year (except in CA 0-52 and NH 0-74)

Minimum premium (flexible premium): $20,000 NQ and Q

Penalty-free withdrawals – up to 10% after Year 1

Premium bonus of 5% on the 10-year and 8% on the 14-year

That premium bonus increases to 7 and 10%, respectively, if your premium is $75,000+!

Interest crediting strategies:

Fixed

Daily Average with Index Margin

Annual Point-to-Point with Cap Rate

Annual Point-to-Point with Index Margin

Annual Point-to-Point with Participation Rate

Monthly Point-to-Point with Cap Rate

Two-Year Point-to-Point with Index Margin

North American Performance Choice and Performance Choice Plus FIA – 8 and 12 Years

Here are a few highlights for the Performance Choice and Performance Choice Plus FIA. (The Plus option has a premium bonus.)

Performance Choice 8 and 12:

Issue ages: 0-85 for 8-year, 0-75 for 12-year

For 12-year: In California 0-52, In South Carolina and Texas 0-55

Premium bonus: 3% on 8-year and 12-year (5% on 12-year in North Dakota) on premium received in first 5 years (may be subject to premium bonus recapture)

10% free withdrawals after Year 1

Interest crediting strategies:

Fixed

Annual Point-to-Point with Cap Rate

Annual Point-to-Point with Margin

Annual Point-to-Point with Participation Rate

Annual Point-to-Point with Threshold Participation Strategy

Monthly Point-to-Point with Cap Rate

Inverse Performance Trigger

North American Strategic Design Annuity X FIA

Here are a few highlights for the Strategic Design Annuity X FIA:

Issue ages 50-79

Single premium, $50,000 minimum Q or NQ

7% free withdrawals after Year 1

Interest crediting strategies:

Fixed

Annual Point-to-Point with Cap Rate

Annual Point-to-Point with Inverse Edge Trigger

Annual Point-to-Point with Participation Rate

Monthly Point-to-Point with Cap Rate

Two-Year Point-to-Point with Participation Rate

Embedded benefits rider (automatically included for .95% annual fee):

Guaranteed lifetime withdrawal benefit (GLWB): GLWB value roll-up of 200 percent of the interest credited expedites potential income growth.

Enhanced penalty-free withdrawals: Annual penalty-free withdrawal percentage starts at 10 percent after the first contract anniversary but can grow as large as 32 percent.

Lifetime income option: Level or increasing options for lifetime payments.

Lifetime payment amount multiplier (may not be available in all states): Doubled lifetime payment amount up to five years, eligibility based on inability to perform two of six activities of daily living (ADLs).

Accumulation value step-up: On the ninth and 10th contract anniversaries, if interest credits are less than the total amount of rider charges incurred the accumulation value will increase by the accumulation value step-up amount.

New to Annuity Sales?

Annuity sales are a huge opportunity for independent agents in the senior market. If you want to learn how to sell annuities to seniors, you've come to the right place!