Clients with a 401(k) or an IRA are perfect candidates for agents willing to sell fixed annuities.

If you haven’t touched annuities, don’t worry – we’re going to cover everything you need to know to get started, including all the little details like transfer forms and RMDs.

If you are an experienced annuity producer, my hope is that you’ll learn something new here and that you’ll be inspired to keep bringing up the conversation with your prospects and clients.

Here’s what we’re going to go over in this article:

- What exactly a 401(k) and IRA are (no stupid questions here!)

- How to easily bring up the tricky subject of money with your prospects and clients

- The 2 major benefits of moving a 401(k) or IRA into a fixed annuity

- The 1 potential drawback of moving a 401(k) or IRA into a fixed annuity

- How the Required Minimum Distribution (RMD) works in this situation

- How and when the 401(k) or IRA money is taxed

- One major mistake I made during the transfer process (learn from my mistakes!)

- The paperwork and forms you’ll need when rolling a 401(k) or IRA into a fixed annuity

- How to address the subject of commission with your client

- How to overcome common objections and worries from conservative and skeptical clients

- The subject of fees when it comes to touching your 401(k) or IRA

It’s a lot, I know, but I want to make sure you’re 100% confident when this subject comes up. If there are any questions you have that are left unanswered, please ask them in the comments section at the end of this article. We do monitor those, and we reply to everyone, so don’t be shy!

New to annuity sales?

Annuity sales are a huge opportunity for independent agents in the senior market. If you want to learn how to sell annuities to seniors, you've come to the right place!

Check out our complete guide here: The Ultimate Guide to Selling Annuities In the Senior Market

What is a 401(k)?

A 401(k) is a retirement savings plan that your employer sponsors, and it’s named after s section of the tax code. A 401(k) helps employees save a portion of their paycheck for retirement before taxes are taken out. The employer will often match a certain percentage of the employee’s contributions. You don’t have to pay taxes on your 401(k) until the money is taken out of the account.

Companies used to offer pension funds, but those costs rose, and many employers turned to 401(k)s instead. There are still government and union jobs that do pensions, but more often that not, we see 401(k)s as the main form of retirement savings.

Most 401(k) plans offer a spread of mutual funds, but the actual setup can vary. There are caveats to having a 401(k), such as being unable to use any of that money for a certain amount of time (also called vesting), and rules about withdrawing your money before retirement age (and fees).

What is an IRA?

An IRA, or Individual Retirement Account, is exactly how it sounds – it’s just a retirement account.

Most of the time, when I’m meeting with clients and they have an IRA, they have a Traditional IRA. This just means that they’ve put pre-taxed money into a retirement account. A common situation is that the client had a 401(k), they retired, and they rolled their 401(k) to another financial institution, like the bank. As soon as that 401(k) is rolled over, it’s now called an IRA.

There is another type called a Simple IRA, but for us agents, we treat these the same way as Traditional IRAs. The only difference is how you mark it on the application.

Finally, there are Roth IRAs, but these are very rare to see as an agent – at least in my experience. I see these maybe 1 out of every 20-25 times. With a Roth IRA, you put taxed dollars (money that has already been taxed) into the account so that when you retire, and you start taking that income, you don’t get taxed. It’s basically a case of ‘get taxed now rather than later.’

How to Bring Up the Subject of Money With Clients

If you’ve read any of my stuff before, I’ll bet you money you can guess how I’m going to approach this subject with my clients.

I’m going to lean on my Client Needs Assessment. I start the conversation by asking the question “Are you satisfied with the current rate of return on your investments?”

Regardless of their answer, I’m asking the follow-up question “Are you dealing with the stock market or are you dealing with the banks?”

And finally, I’m covering all my bases by asking a final question: “Do you have a 401(k)?”

I have seen agents fill out their Client Needs Assessment and then stop when it comes to the “money” questions. I completely understand – we’re often taught that talking about money is a no-go subject, but when you have conviction that you can really help the client, you have to push yourself to get over that discomfort.

It pains me to see so many lost opportunities because the agent is afraid to talk about money.

The 2 Major Benefits of Moving a 401(k) or IRA Into a Fixed Annuity

I do want to clarify right away that I’m recommending a fixed annuity – NOT a variable annuity. This is important, because the rest of the article does not apply if you’re trying to sell a variable annuity – which we DO NOT recommend. (You can see I’m pretty passionate about this.)

However, the 2 major benefits of moving a 401(k) or IRA into a fixed annuity are:

- The client has someone looking out for their investment

- Their retirement savings are safe and secure

If the client is almost 65 and they have a 401(k) with their employer, once they retire, no one is contributing to it anymore. They won’t have anyone looking out for their investment, because they’re no longer an employee there. That 401(k) may do well and it may not do well, but oftentimes, the client gets a monthly statement and they don’t understand what it is.

Clients want a more hands-on approach, and they want to know what’s going on with their investment. I can’t tell you how many times I’ve sat down with a client, and by the end of my presentation, they’re just in shock and awe that they finally understand how all of this works. That makes my job worth it.

The second benefit is safety. When a client retires, they’re moving from an accumulation stage to a preservation stage. When we move into the preservation stage, we have to adjust our investment strategy.

You want to be more conservative and put safety as a higher priority over risk. Safety first, competitive interest rates later.

The 1 Major Drawback of Moving a 401(k) or IRA Into a Fixed Annuity

The only drawback of rolling a 401(k) or an IRA into a fixed annuity is when the client doesn’t know how much money they plan to take out and when they plan to use it.

It makes it really difficult to recommend a fixed annuity for that type of client, because they’d be locking in a guaranteed contract for 5 years. Even though they can have a 10% free withdrawal, it may or may not be enough.

For example, if the client wants to buy a new car and they need more than 10% of their investment, that would be a big drawback.

As an agent, you want to be asking this question before ever recommending a fixed annuity: How much money will you need to access within the next 5 years?

Most of the time, the common answer is this: “Well… you know… I’m told that I’m supposed to start taking it out at some age, but I don’t know that we’ll need it.”

And that brings us to another important topic, which is the Required Minimum Distribution (RMD).

How Does the Required Minimum Distribution (RMD) Work?

You generally have to start taking withdrawals from your IRA, SIMPLE IRA, SEP IRA, or retirement plan account when you reach age 70½. Due to changes made by the SECURE Act, if your 70th birthday is July 1, 2019 or later, you do not have to take withdrawals until you reach age 72.

So, once the individuals turns the appropriate age, those withdrawals must begin no later than April 1 of the following year.

Read more about RMDs on the IRS website

Now, one important thing to note here is that your client only has to take out the Required Minimum Distribution (RMD) on pre-taxed money. That’s the whole purpose of the RMD existing.

So, if they’re starting up an annuity with money that has already been taxed (say, money from their savings account or a Roth IRA – which was taxed in the beginning), they don’t need to pay attention to the RMD.

Is Rolling a 401(k) or IRA Into a Fixed Annuity a Taxable Event?

If you roll your 401(k) into a fixed annuity, it’s a non-taxable event, because you’re not withdrawing the money for yourself – you’re just transferring it from one retirement vehicle to another.

It’s not considered a distribution – you’re simply saying that you want your 401(k) to be rolled over to another financial institution, which means it’s still tax-deferred. In essence, your client is saying that they just found a better retirement savings vehicle with better interest, safety, and security.

One Major Mistake I Made During the Transfer Process

OK, so we’ve established that rolling a 401(k) or IRA into a fixed annuity is a non-taxable event. Well, I made a mistake with this once, and I want you to learn from the nightmare that followed.

I tried to do a transfer with a client named Mr. Wallas. Legally, the company that holds the money has a certain amount of time that they can hang on to that money before they're required to transfer it. The company was dragging their feet big time, and they wanted the client to jump through all these hoops to do the transfer.

So, to speed things up, we had the client take out the money himself in order to complete the transfer. Well, this was the problem – the company made the check out to Mr. Wallas – not the new financial institution. So, even though we rolled that money into another financial institution immediately, it was technically a withdrawal, and Mr. Wallas was taxed on the entire amount.

Everything that we did was fine, but the issue occurred when the bank made the check out to Mr. Wallas, not the insurance company.

He wasn’t happy.

So – please make sure that the the check is never made out to the client – make sure that it's made out to the insurance company. Never have a client make a personal withdrawal from their retirement account. Otherwise, they'll be taxed on the amount, which can be avoided.

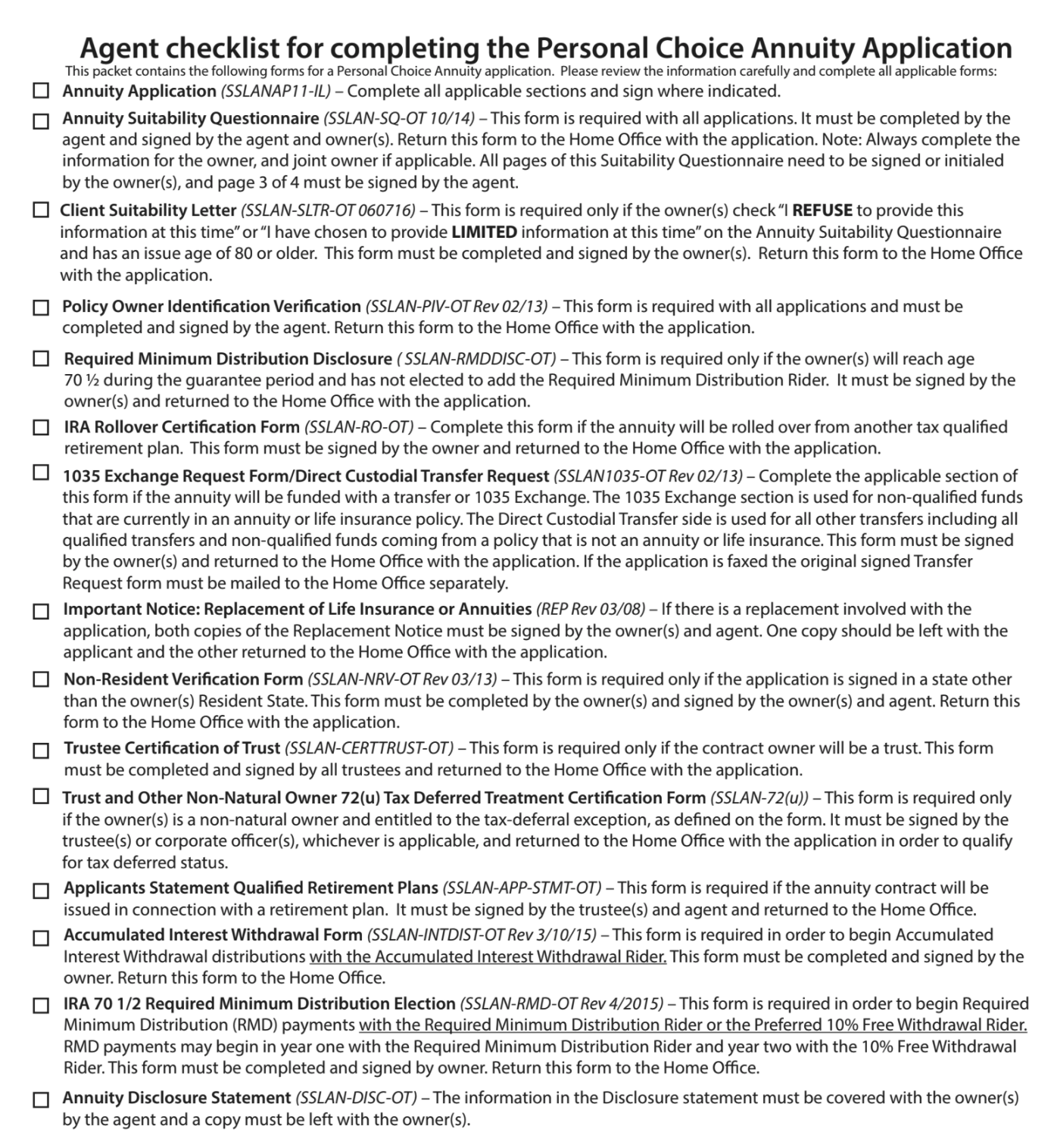

What Forms and Paperwork Does the Agent Need to Be Aware Of?

All the companies we represent do a great job of including every form you need in their application kit.

There are some companies who just give you an application, and if you are transferring an IRA for example, you’d need additional forms.

In most cases, you need to fill out a transfer form, but don’t get caught up in this. You can contact our office for support at any time, and we’ll make sure you have all the paperwork you need.

Check Out Annuity CompaniesHow to Address the Subject of Commission With Your Client

Commission is often a point of concern for clients, because they think they’ll have to pay a fee for it. We know that with fixed annuities, this isn’t the case, and here’s how I explain this to my clients.

I tell them that 100% of their account value earns a guaranteed interest rate. They will never ever see a fee taken out of their account value for my commission. Basically, they will never see anything that reduces their account value because they have an agent.

I receive a commission from the company we write the product with, but it does not impact the client’s policy at all. It’s just like another other health insurance policy.

Now, again, we are talking about FIXED annuities. Don’t confuse any of this with variable annuities.

How to Overcome Common Objections From Skeptical Clients

When you walk the client through the entire process, you are naturally going to wow them with the information that you know. You clearly know what you’re talking about, and the client realizes that you’re an expert.

So, my main advice here is to put it all out there. I show my client every single part of the process, and I take the lead role. I give the presentation, and I take it a step further and don’t wait for the client to ask any questions – I answer everything up front. I explain the details of the transfer process including the transfer form, how the RMD works, etc.

If you can be proactive in answering all of this during your presentation, I think you’ll find that your clients will just be amazed and relieved – not full of objections and skeptical questions.

What Do You Say When the Client Asks About Fees?

I don’t blame anyone for being hesitant when we talk about touching their life savings. But here’s the fact of the matter: it’s highly unlikely that there are any fees involved in rolling over a 401(k).

You can always check on this, but it’s just not a typical scenario, so there’s really nothing to be concerned about. You just have to help your client feel confident that you’re making a solid recommendation – which you are!

What Next?

Now, it’s time to start bringing up this subject with your prospects and clients.

Leave it up to the Client Needs Assessment – it takes the pressure off of you, and it helps start the conversation.

You can also take a look at the current fixed annuity rates (which have just increased, by the way). The annuities that stand out to us as very competitive are highlighted in yellow. We also have a 5-Year Annuity Tip Sheet that's very handy and updated regularly when new rate changes are announced:

If you feel like you need more guidance, please contact our office!

Have you ever rolled a 401(k) into a fixed annuity?

Updated May 27, 2020 with the new information from the SECURE Act regarding Required Minimum Distributions